“One Big Beautiful Bill Act” OBBA: Key Provisions for Individuals

You have likely heard news about the “One Big Beautiful Bill Act (OBBBA),” also known as the 2025 Tax Act. You naturally may have questions about what this new legislation entails and how it might impact your 2025 tax return. The OBBBA represents the most significant legislative overhaul of the tax code in several years. This act made several key provisions of the 2017 Tax Cuts and Jobs Act (TCJA) permanent and introduced several new, significant deductions and credits. Keep reading to find out more!

First, let’s cover something simple, the standard deduction. For tax year 2025, the standard deduction amounts will increase:

- Married Filing Jointly: $31,500 (This is a $2,300 increase over 2024.)

- Single / Married Filing Separately: $15,750 (This is a $1,150 increase over 2024.)

In addition to these increases, the Act introduces a new, temporary $6,000 deduction for individuals aged 65 and older, available for tax years 2025 through 2028. This deduction is subject to an income phase-out beginning at $75,000 for single filers and $150,000 for joint filers.

Looking ahead to 2026, we will see an increase of about 2.2% in the standard deduction – making it $16,100 for single-filers and $32,200 for joint.

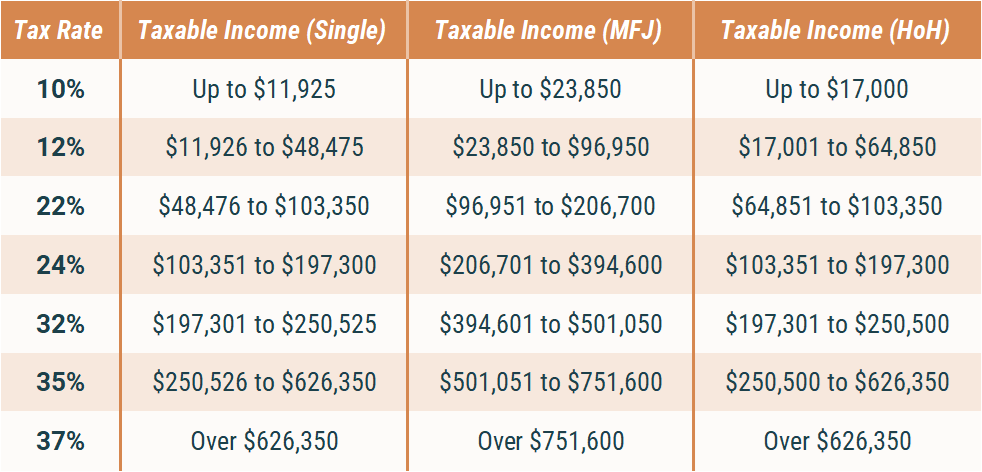

Other Individual OBBA Updates

Tax Rates: The 2017 tax rates (as pictured in the tax rate table) are now permanent.

- Increased SALT Deduction Cap: For tax years 2025 through 2029, State and Local Tax (SALY) deduction cap is increased from $10,000 to $40,000. The cap applies to all filing statuses and is subject to a phaseout. The phaseout begins for taxpayers with an AGI of $500,000. The cap for taxpayers with AGI of $600,000 or higher returns to $10,000.

- “No Tax on Overtime” Deduction: A new deduction is available for qualified overtime pay, up to $12,500 for single filers and $25,000 for joint filers (subject to phaseouts).

- New “No Tax on Tips” Deduction: A new deduction allows for up to $25,000 in tips to be excluded from income for certain occupations, subject to income phaseouts.

- New Vehicle Loan Interest Deduction: A new deduction is available for interest paid on loans for new personal-use vehicles.

- Child Tax Credit (CTC): The CTC is $2,200 per qualifying child. The refundable portion of the credit (the Additional Child Tax Credit) is capped at $1,700.

- End of Clean Vehicle Credits: The law permanently eliminates the tax credits for new and used clean vehicles (including electric vehicles) for purchases made after September 30, 2025.

Charitable Contributions

This has become one of the most effective ways for individuals to utilize personal expenses as a tax deduction. Since the passage of the TCJA, most personal expenses are either subject to limitations (medical and taxes) or are non-deductible. If you find yourself in a high-income year, or are on the cusp of itemizing, consider increasing donations.

While the charitable contribution deduction remains unchanged for 2025, there are big changes on the horizon for tax year 2026:

- New Deduction for Non-Itemizers (The “Universal Charitable Deduction”) Taxpayers who take the standard deduction will be able to deduct a portion of their charitable gifts (up to $1,000 for single filers and $2,000 for MFJ filers.)

- New “Floor” for Itemizers: You will only be able to deduct the amount of your charitable contributions that exceeds 0.5% of your AGI. (Example: If your AGI is $200,000, the 0.5% “floor” is $1,000. If you donate $5,000 to charity, you will only be able to deduct $4,000 (the amount over the $1,000 floor).

New “Cap” on Benefit for High-Income Earners: Also starting in 2026, the value of the deduction for those in the 37% tax bracket will be capped. The tax benefit for all itemized deductions (including charitable) will be limited to 35 cents on the dollar. (Example: A taxpayer in the 37% bracket who makes a $10,000 donation will receive a $3,500 tax benefit (35%), not the $3,700 (37%) they would have received under the old rules).

OBBA: Key Provisions for Business Owners and Investors

- Qualified Business Income Deduction (QBID): This deduction is now permanent. It was scheduled to expire after 2025.

- 100% Bonus Depreciation: The OBBA restores and makes permanent 100% first-year bonus depreciation. Previously, this was subject to a phasedown. The new law applies to assets placed in service after January 19, 2025.

- Section 179 Expensing Enhanced: Expense limit increased to $2.5 million and phaseout threshold increased to $4 million.

2025 Retirement Plan Adjustments

The IRS has released the 2025 inflation-adjusted limits for retirement and health savings plans. OBBA did not impact these, but the new “Super Catch-Up” from the SECURE 2.0 Act takes effect.

- 401(k) Contribution Limits: The maximum employee contribution for 2025 is $23,500.

- Age 50+ Catch-Up: The standard catch-up contribution for those aged 50 or older remains $7,500. The total contribution for this group (age 50-59 and 64+) is $31,000.

- NEW “Super Catch-Up” (Age 60-63): Effective in 2025, a provision from the SECURE 2.0 Act allows for a higher catch-up for participants aged 60, 61, 62, and 63. This “super catch-up” is $11,250. This amount replaces the $7,500 catch-up, and is not in addition to it. The total maximum contribution for this age bracket is $34,750 ($23,500 + $11,250).

IRAs

Don’t have a retirement plan through your employer? Consider making traditional or Roth IRA contributions. Contributions to traditional IRAs are tax deductible, grow tax-free, but are taxable when withdrawn. Contributions to Roth IRAs, on the other hand, are NOT deductible but these receive tax-free growth and are not taxable when withdrawn. If you are in a high-income year or expect to be in a lower tax bracket when you retire, traditional IRAs often make more sense. If you are in a low-income year or expect to be in a higher tax bracket when you retire, Roth’s are a common way to go. Converting your traditional IRAs to Roth IRAs are also worth considering in low-income years.

IRA Contribution Limits: The 2025 contribution limit for Traditional and Roth IRAs is $7,000. The age 50+ catch-up contribution remains $1,000, for a total maximum contribution of $8,000.

HSA Contributions

Contributions to health savings accounts have increased to $4,300 (self-only) and $8,550 (Family), up from $4,150 and $8,300 in 2024, respectively.

2025 Annual Gift & Estate Limits

The IRS has announced the 2025 inflation adjustments for wealth transfer:

- Annual Gift Exclusion: For 2025, the annual gift tax exclusion has increased to $19,000 per recipient.

- Married Couples: A married couple can combine their exclusions to gift $38,000 per recipient, per year, without filing a gift tax return or using any lifetime exemption.

- Lifetime Exemption: The lifetime gift and estate tax exemption has increased to $13.99 million per individual for 2025 ($27.98 million for a married couple). Unless Congress acts, his exemption is currently set to be cut in half, to $7 million per person, on January 1, 2026.

- Direct Payments: Payments made directly to an educational institution for tuition or directly to a medical provider for medical expenses do not count against either the $19,000 annual exclusion or the $13.99 million lifetime exemption.

Long-term Capital Gains Tax Rates

Like the tax rates, the long-term capital gains rates income thresholds were adjusted for inflation.

In 2025, the 0% rate applies for individual taxpayers with taxable income up to $48,350 on single returns ($47,025 for 2024), $64,750 for head-of-household filers ($47,025 for 2024), and $96,700 for joint returns ($94,051 for 2024).

The 20% rate for 2025 starts at $533,401 for singles ($518,901 for 2024), $566,701 for heads of household ($551,351 for 2024), and $600,051 for couples filing jointly ($583,750 for 2024).

The 15% rate is for filers with taxable incomes between the 0% and 20% breakpoints.

The 3.8% surtax on net investment income stays the same for 2024. It kicks in for single people with modified adjusted gross income over $200,000 and for joint filers with modified AGI over $250,000.

Qualified Charitable Distributions

Are you required to make distributions from your IRA but don’t want to? If you are 70½ or older, you have the option to transfer up to $108,000 of your IRA distribution to a charity. Any donation amounts up to $108,000 are treated as non-taxable to you. Additionally, if you are 72 or older, your QCD counts toward your required minimum distribution for the year.

529 Plan Contributions

These plans are a great way to save for future education costs. While contributions to these plans are not deductible on your federal return (many states, including Arizona, have a deduction) the money grows tax-free and distributions for qualifying educational expenses are not taxable. And, in addition to higher education costs, funds in these accounts can be used to cover private school tuition of up to $10,000 per year.